Building efficiency through partnerships

Marmon Utility President Ken Woo highlights how the company has been delivering electric infrastructure supports for 75 years

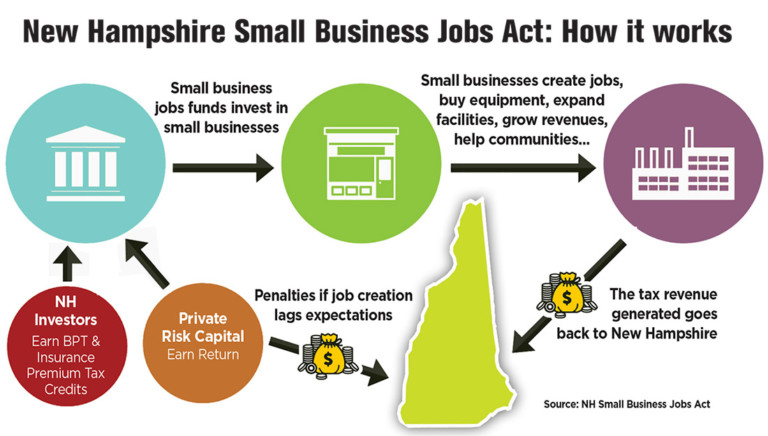

Would a proposed NH Small Business Jobs Fund create so much economic activity through tax credits that it could reverse rush hour traffic on Interstate 93, as one lobbyist put it, or are such programs a “scam” to let out-of-state investors raid the state treasury? Or is the answer somewhere in-between?

For the Granite State, those — literally — are the $60 million questions. And, because they revolve around a program that would be such a quantum leap beyond anything that the state has ever done in terms of funding economic development, after sailing though the Senate as Senate Bill 205, it ran aground in the House Ways and Means Committee, which on April 21 retained it until next year.

Stormy controversy seems to follow such complicated tax credit programs, which have spread to some 14 states over the past few decades.

That’s especially the case in Maine, which will give out $16 million in tax credits to Portsmouth-based Cate Street Capital for a project involving the former Great Northern Paper Mill that went bankrupt.

But while both sides on the New Hampshire proposal attack each other — sometimes personally — there are larger philosophical questions as well. Should New Hampshire, with no history of providing business tax giveaways, join the national bidding war in such a big way? And if it does, should it set up a program giving the state more oversight, at the risk of “picking winners and losers,” or should it leave that in private hands, even though the public’s tax dollars might be at risk?

James Key-Wallace, executive director of the NH Business Finance Authority said he isn’t opposed to the purpose of the program, but he did question whether it would be the best way to achieve its goals.

“The state would be well advised to perform an evaluation of options, with an informed and impartial view of the pros and cons for each approach,” said Key-Wallace. “Failure to do so properly could cost the taxpayers up to $60 million, with potentially having nothing to show for it.”

But to backers of the Small Business Jobs Act, very little is at risk. It is a program that, by design, not only pays for itself, but raises millions of more dollars and creates thousands of jobs.

Revenue-neutral?

Here is how SB 205 is supposed to work:

The state would offer as much as $60 million in dollar-for-dollar tax credits against state business taxes. The applicant — from among 89 eligible federally approved specialized equity funds — would raise $40 million, including $10 million of their own capital to create a $100 million pool. That pool in turn could give out “non-bankable” loans or investments of up to $5 million to nearly any “growth” company — a firm with less than 250 employees and less than $10 million in revenue — which would hire low-to-moderate-income people or are located among them.

The eligible businesses should be involved in manufacturing, plant sciences, agribusiness, mining, clean energy, cybersecurity, information technology, defense, life sciences and biotechnology, but the state Department of Resources and Economic Development could deem any other potential industry “highly beneficial to the economic growth of the state” as well. (DRED would have to determine if it would create enough jobs to generate enough state taxes to pay for the credits.)

Indeed, the credits won’t actually be granted until the third year of a four-year period, after all the investments have been made. And if job targets are met, the investors pay a portion of their profits to the state.

“So it should be revenue-neutral to the state,” said Sen. Jeb Bradley, R-Wolfeboro, who testified for the bill before the House Ways and Means Committee on April 12, “It is just another opportunity in our quiver to promote jobs and small business.”

Major departure

And it would be a particularly important tool for continued growth of New Hampshire companies, according to Stephen Bennett, managing director of Stonehenge Capital Company LLC, and Jeff Craver, a principal of Advantage Capital Partners. The two firms are among the 89 Small Business Investment Companies (SBIC) with a large enough portfolio ($100 million) to be eligible under the proposed law to manage the investment pools, for a fee. None of the companies are based in New Hampshire, though Advantage Capital has an office in Hanover.

In a white paper presented to the committee, the two executives made the case that while the state has a number of programs for startups (including the recently announced public-private Millworks II fund), it lacks the venture capital firms and angel investors that can take companies to the next level.

And they brought in John Andreliunas CEO of Quoddy — a high-end shoe manufacturer based in Lewistown, Maine — to talk about the $500,000 loan that helped his company retain 27 jobs. The funding allowed it to pivot from a wholesale distribution to a more profitable direct made-to-order sales model.

“We had nowhere to turn,” Andreliunas told NH Business Review. “We talked to banks who were very nice, but no one wanted to lend us money unless we had money.”

But House committee members seemed to doubt the need for a massive jobs program.

“With the unemployment rate, are there really that many people to hire?” asked Rep. Charlie Burns, R-Milford.

That skepticism extended to the entire program, especially after hearing from both Key-Wallace of the BFA and Carollynn Ward, tax policy analyst with the state Department of Revenue Administration.

Such a program would be a major departure for the state, Ward said. The research and development tax credit is the largest tax credit on the books, and lawmakers wrung their collective hands when they expanded it from $2 million to $7 million last session.

Secondly, even if the program did create the jobs promised, “there are no guarantees that you will be recouping your revenue,” she said. That’s because New Hampshire is not an income tax state, so an extra job only translates into business enterprise tax revenue, currently at a 0.72 of one percent of payroll, and going down.

Craver of Advantage Capital contested the one-to-one credit criticism, noting that some investors won’t get any tax credits, so it was really more like a 50-50 match.

As for revenue generation, that doesn’t count indirect economic activity. Growth would mean larger profits, resulting presumably in more business profits tax revenues, and the resulting spending would pump through the economy, pushing up rooms and meals tax and real estate transfer tax revenues, he said.

Shadow over Maine program

But all of this — even the number of jobs created — is difficult to measure.

“Who provides oversight to determine that the ‘created jobs’ would not have occurred in part or whole without the investment? What is the methodology for counting these jobs?” asked Key-Wallace.

For instance, Maine’s audit of a similar program — the New Market Capital Invest Program — concluded that $76 million in tax credits generated 764 permanent jobs, but it also credited the program with retaining 257 “temporary jobs” at the Great Northern Paper mills that were actually layoffs.

Other audits counted layoffs as a minus, but Craver in one retort said that was “ridiculous,” since the investment didn’t cause the job loss, just prevented it from happening sooner.

The Great Northern investment cast a shadow over the entire Maine program, leading to an investigation by the Maine Sunday Telegram that dug into the complex $40 million investment transaction orchestrated by both Stonehenge and Enhanced Capital Maine GNP LLC, another SBIC, to revive the mill in East Millinocket.

“The reality is most of that $40 million was a mirage,” summed up the article.

It turns out that investors used several accounting tricks, including a $31.8 million one-day loan for a Cate Street Capital subsidiary to buy paper machines and equipment from another Cate Street subsidiary to “artificially inflate” the value of the investment to receive the maximum amount of tax credits, the paper charged. The move resulted in $16 million of tax credits, which resulted in about $2 million in brokerage fees for the SBIC. Cate Street has declined comment to NH Business Review.

The $8.2 million money that did get to the mill was used to refinance existing debt, but was not enough to prevent bankruptcy, the article stated.

There were other factors that caused the bankruptcy, of course, and, as Craver pointed out, it is unfair to concentrate on one failure in a program that has made 5,500 investments.

He pointed to the official Maine audit, which, while faulting the one-day loan loophole in that and other investments, noted that as a whole the $76 million in tax credits attracted $130 million in private investment, and resulted in an overall positive $16 million positive fiscal impact.

But to look at the report another way, that $1 in investment, resulted in $1.19. And it cost nearly $100,000 to create or retain each job.

Was it the most effective return on the investment?

“If I stood on a street corner and handed out $20 bills, that would be an economic stimulus, but would that be the best way to do it?” asked Julia Sass Rubin, an associate professor at Rutgers University’s Edward J. Bloustein School of Planning and Public Policy, and a frequent critic of such programs.

The state of Florida, which also has a New Markets Development Program, did attempt to look at the return on investment various tax incentive programs. The state paid out $64.3 million and got back 1.8 percent in 2017. That was the third-highest pay out of the seven programs evaluated for that year. The best yielded a 4.4 percent return.

Similar programs didn’t fare well in other state evaluations, according to another investigation, conducted by the Pew Charitable Trusts in early April. That study examined audits in six other states, concluding that the programs “failed to deliver promised jobs and tax revenue”.

The Pew report gave the House committee “considerable disquiet,” said Rep. Susan Almy, D-Lebanon. “It seemed that the state is taking all the risk and the investors were getting a lot. It works out for the business side just fine.”

Craver dismissed such reports. He said Pew itself is suspect because it lobbies the government and charged that state reports quoted in the Pew report are either outdated or were written too early in the program to measure the full benefits.

And, he said, all of the experts quoted in the Pew investigation were “members of groups that have lobbied against economic development incentives and public-private partnerships while pursuing their own, competing policy agendas.”

He said several were members of conservative think tanks who are leery of government spending, while Rubin of Rutgers was hired by the state of Maryland for a competing program and faced ethic complaints.

Rubin replied that Maryland paid her $2,500 as a consultant to evaluate a program that had nothing to do with New Markets Tax Credits, and the ethics violation had to do with a charter school association that she said was dismissed.

This is an example, she said, that proponents of such programs “will do anything to discredit those who speak up.”

Oversight questions

Craver also said that New Hampshire has various safeguards that protect state taxpayers — safeguards that earlier versions of the program didn’t have. The one-day loans that plagued Maine, for instance, are not allowed under the New Hampshire bill. And there are “strict clawback provisions” that would result in investors losing a portion of profits if goals aren’t met.

Lawmakers like Bradley were satisfied with these provisions. But House members weren’t so sure. “What if there weren’t any profits?” said Almy.

If there were, investors still would keep most of it. If less than 60 percent of the jobs were created, investors would hold onto 70 percent of profits. And those receiving the tax credits would still receive all of them.

And, said Key-Wallace, “there is no oversight related to how the funds lend or invest their money once they receive it.”

But Robert Clegg, a lobbyist for Advantage Capital, questioned Key-Wallace’s testimony.

“The BFA testimony is full of inaccuracies,” said Clegg. “They are just upset that they are not steward of the money.”

Key-Wallace denied this.

“The Business and Finance Authority is a completely self-funded entity and would like to remain that way. The only reason we chimed in was that we were asked to and have the technical expertise to evaluate it.”

Clegg, collected a $12,000 fee for his lobbying efforts this year, but that is not the reason he supports the bill. It does protect the state and lays the risk on the investors, he said.

“The New Hampshire bill is the strictest bill of them all,” he said.

It would make capital available at the single-digit level, much less than most current government-sponsored finance programs, he said. And it would draw business and good-paying jobs up to the Granite State.

“It would reverse the commute to Massachusetts,” said Clegg. “They’ll be driving north every morning.”

Marmon Utility President Ken Woo highlights how the company has been delivering electric infrastructure supports for 75 years

Gather’s new culinary education program, Fresh Start, is a way to teach people with employment challenges the kitchen skills and life skills they need to have a career in the food service industry

Artificial intelligence is transforming business at remarkable speed. Most discussions focus on productivity gains, cost savings or the jobs AI may eventually replace. Yet a more significant change is already underway — one that could reshape the future of nearly every profession.

Good news for patients — and a reminder of what’s at stake

New Hampshire businesses are facing a workforce challenge that goes beyond wages and hiring.

5 tips for creating an estate plan that reflects all of your legacy

Business and event happenings around the state of NH

The Latest is a roundup of the comings and goings of the movers and shakers in NH's business community

Unapproved and unmonitored AI use is spreading inside businesses faster than leadership teams know, and it may be one of the biggest privacy and security blind spots companies have today.