New state law empowers homeowners with ‘balcony’ solar panels

With a new state law set to go into effect with the dawn of a new year in 2027, Granite Staters will be able to install so-called “balcony solar” panels for home use.

Raising children is one of the most meaningful and rewarding things people do, and there are major financial implications that come with a growing family.

For the parents of a newborn today, the future annual cost of a college education may run more than $70,000 per year at a moderately priced private college and more than $35,000 per year at a public university offering in-state tuition discounts, once we factor in inflation.

Believe me, having three young kids at home and a fourth on the way, I know how expensive it is to raise children. The best thing one can do is to start planning early and make adjustments as time goes by.

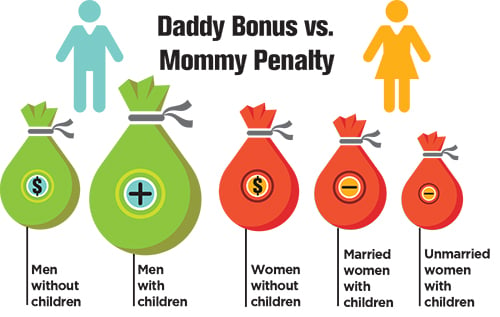

A recent Wall Street Journal article reported that men without children earned 40 percent less than men who are fathers. This was referred to as the “daddy bonus.” The article didn’t specify whether men with kids are motivated to work harder to provide for their family or whether companies reward fathers with better positions assuming they are more disciplined and focused due to their commitment at home. Either way, the median income for fathers is significantly higher than for men with no children in the study.

Unfortunately, for women there is a “mommy penalty,” as working moms earn less than women without children. However, married working moms are seeing this penalty slowly disappear while unmarried working moms are experiencing the penalty increase.

Beyond the cost of putting kids through college, there are so many other expenses associated with raising children. The cost of diapers, birthday parties, field trips at school, after-school activities, sports, cellphones, food, family travel, etc., is estimated to add up to more than $500,000 through age 18. (I am sure the fathers reading this are hoping for an even bigger “daddy bonus” to cover the cost of their children.)

A popular savings vehicle for parents who are planning for their kids’ college education expense is the 529 Plan. Distributions from 529 Plans are exempt from federal income tax if used for qualified higher education expenses like tuition, room, board and books. The plans offer a great option for parents to save, as they include tax benefits in addition to the convenience of the investment account. The accounts can be owned by parents, grandparents or others who want to help save toward higher education. Contributions can be made monthly, quarterly, annually, or just when funds are available. Low-cost plans from American Funds are highly rated and available through Registered Investment Advisors. Vanguard is another popular company offering a low cost 529 Plan. There are no income limitations to making contributions to 529 Plans, like there are with some other savings accounts.

The first few months of having a new baby at home can be chaotic at times as everyone adjusts to the random needs of their baby. Parents have so much to focus on to ensure their long term success.

Daniel Cohen, CEO and chief investment officer at Cohen Investment Advisors, Bedford, can be reached at 603-232-8351 or through investwithcohen.com.

With a new state law set to go into effect with the dawn of a new year in 2027, Granite Staters will be able to install so-called “balcony solar” panels for home use.

Marmon Utility President Ken Woo highlights how the company has been delivering electric infrastructure supports for 75 years

Gather’s new culinary education program, Fresh Start, is a way to teach people with employment challenges the kitchen skills and life skills they need to have a career in the food service industry

Artificial intelligence is transforming business at remarkable speed. Most discussions focus on productivity gains, cost savings or the jobs AI may eventually replace. Yet a more significant change is already underway — one that could reshape the future of nearly every profession.

Good news for patients — and a reminder of what’s at stake

New Hampshire businesses are facing a workforce challenge that goes beyond wages and hiring.

5 tips for creating an estate plan that reflects all of your legacy

Business and event happenings around the state of NH

The Latest is a roundup of the comings and goings of the movers and shakers in NH's business community