NHBR About Town: Week of June 19, 2026

Business and event happenings around the state of NH

In August, President Bush signed into law the Pension Protection Act of 2006, the most comprehensive retirement benefits reform act in at least a decade.

While the act affects nearly every type of retirement arrangement, as well as a large number of unrelated tax issues, many of its most significant provisions are those affecting defined benefit pension plans – the types of plans our parents used to have, and many unionized employees still do. They promise to pay employees a predetermined amount of income, for life, after retirement.

The act radically changes the manner in which pension plans are funded and ultimately requires higher funding levels, albeit using methods that are clearer and easier to understand than under the old law. These changes will have a major impact on decisions employers must make about pension plan design, funding and even whether to continue or start a pension plan.

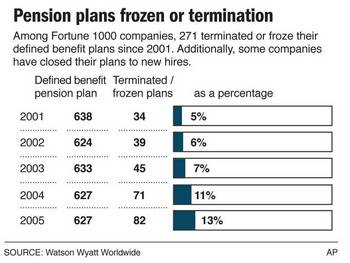

In the act, Congress has addressed what many perceive to be the two main problems facing pension plans: the dramatic underfunding of the trusts established by employers to pay pension plan benefits; and the lack of options available to employers of existing pension plans who determine that they can no longer afford to maintain their plans under the existing rules.

Congress understood that these two problems stifled the creation of new pension plans and forced the freezing or termination of many existing pension plans just at a time when the willingness of Americans to save for themselves has hit an all-time low. It sought to fix these problems by adopting new pension funding rules and adding provisions intended to make it easier for businesses that sponsor existing pension plans to keep them in place.

New rules

Common sense suggests that the only real solution to the funding problem is to require employers to put more money into their pension plans. The trick for Congress was to find a way to do this that did not kill off existing pension plans. Congress appears to have found a solution that achieves both goals.

In the past, the formulae that determined the range of annual contributions an employer could or must contribute to a pension plan were subjective, highly volatile and ultimately failed to provide for safely funded pension plans. Prior to adoption of the act, the funding target mandated by law was 90 percent of a plan’s predicted financial needs. Consequently, an underfunded pension plan was not only permissible, but was the target itself.

Over time, the act will require higher overall contributions, but will remove much of the subjectivity and volatility that resulted under prior law, and will encourage additional contributions in years when the employer can afford them.

The act accomplishes these goals by mandating that certain actuarial assumptions used to predict the future cash needs of a pension plan fall within a prescribed range, and by disregarding short periods of particularly good or bad investment performance. These changes, coupled with increased availability of tax deductions for higher contributions, should result in a “smoother” series of contributions, a corresponding increase in the predictability of the annual required contributions, and more fully funded pension plans.

Thus, Congress seems to hope that greater predictability and less confusion over funding requirements will offset higher eventual funding standards, with 100 percent funding, rather than 90 percent, being the new goal.

More employer options

The act does a good job of addressing the problem of what employers who sponsor pension plans can do once they become too burdensome to maintain.

First, it confirmed what the 7th Circuit Court of Appeals had decided for IBM just days earlier — that the conversion of a pension plan into a “hybrid plan” is not inherently discriminatory against older workers.

A hybrid plan is a type of pension plan that expresses its benefits, and to some degree determines its contributions, in the form of a theoretical account balance based on the projected benefit that would be available to a participant if he or she remained employed until retirement age. Until some federal courts had begun ruling in the first half of this decade that such conversions were, by definition, discriminatory, these hybrid plans had been an increasingly popular option for plan sponsors that wanted to avoid the complex funding requirements applicable to traditional pension plans, and wanted to boost employee morale by offering a pension benefit that allowed employees to see their pension plan benefit growing over time in the same way that they could with a 401(k) plan or an IRA.

Fortunately for sponsors of pension plans who are or may be considering conversion to a hybrid plan, the act went further than simply authorizing these conversions. It laid out clear tests that must be satisfied in order to implement a nondiscriminatory conversion to a hybrid plan, and also amended the Age Discrimination in Employment Act in order to prevent further challenges to these conversions.

Moreover, the act specifically overruled the holding of some courts that sometimes resulted in hybrid plans being required to pay participants lump sums in excess of the employee’s accrued account balance.

In addition, and probably because hybrid plans resemble 401(k) plans and similar profit-sharing plans, the act requires that hybrid plan benefits become nonforfeitable on the same schedule as benefits provided under 401(k) and similar defined contribution plans (generally after three years). This is a faster schedule than that required of other pension plans (generally five years).

The act has ended the uncertainty that caused many employers who sponsor pension plans to adopt a “wait-and-see” attitude. These employers must now carefully consider how the act will affect the funding and operation of their pension plans in the future.

Employers who elect to maintain traditional pension plans can expect to see rising contribution requirements, a burden that may or may not be offset by the increase in cash-flow predictability and more adequately funded plans. Employers who may have frozen accruals under their traditional pension plans or who have been waiting for guidance concerning conversions to hybrid plans now have the authority to develop and implement a plan of conversion that will meet both their needs and those of their employees.

In either case, pension plan reform has arrived, and affected employers will need to decide quickly, and with a full understanding of the details of the act, how they will respond.

David H. Phillips, an associate with the Concord-based law firm of Gallagher Callahan & Gartrell, focuses on the areas of taxation and employee benefits. Prior to joining the Gallagher firm, he worked for eight years in the financial services industry providing plan design and compliance advice to both qualified and nonqualified defined contribution plan sponsors.

Business and event happenings around the state of NH

The Latest is a roundup of the comings and goings of the movers and shakers in NH's business community

A brand new and redesigned Revo Casino and Social House came back to Manchester’s land-use boards this month after the acquisition of additional nearby properties allowed the creation of an expanded vision for the project.

The New Hampshire House and Senate sent three bills to Gov. Kelly Ayotte intended to enable more housing construction, overcoming opposition from the New Hampshire Municipal Association and others.

HEALTH CARE By: DR. STEVEN ANGELO As more Americans live longer, maintaining brain health is becoming an increasingly important part of overall well-being. During Alzheimer’s & Brain Awareness Month, and throughout the year,…

Small and medium-sized enterprises (SMEs) make up the majority of businesses in NH and play a vital role in driving economic growth, innovation and job creation.

Keene’s downtown infrastructure project will tentatively break ground in Central Square on July 6, Keene’s public work director said last Wednesday.

Successful investing takes a lot of patience. Risk tolerance and time horizon are important factors in determining an appropriate investment strategy. For example, some investments would be unwise to choose if the principal is…

From left, former Yankee Publishing CEO Jamie Trowbridge; Granite VNA President and CEO Beth Slepian; CASA New Hampshire President and CEO Marty Sink; President and CEO of the Palace Theatre Trust Peter Ramsey; and President and…