One week into the securities fraud trial of five former Enterasys Networks executives, a defense attorney was questioning whether a witness was only cooperating to avoid spending “a big chunk” of her life in prison.

At the time, U.S. District Judge Paul Barbadoro seemed to imply that this was a bit of exaggeration.

“I mean, you are not talking decades in prison for everybody here, are you?” he asked Assistant U.S. Attorney William Morse.

“I don’t think so your honor,” replied Morse.

“I mean, this isn’t WorldCom or Enron,” Barbadoro said.

But more than six months later, three of the four executives convicted in that trial actually did face spending decades in prison, comparable to the longest sentences handed out to executives in the multibillion-dollar WorldCom and Enron securities frauds. The Enterasys executives ended up waiving their right to appeal – plea-bargaining, in effect, after the fact – so they would serve “only” about a decade apiece for a conspiracy that took place six years ago.

The sentences could have been far worse under current, get-tough-on-corporate-crime sentencing guidelines that were in place after the conspiracy began.

“These guys are lucky to have committed their crimes when they did,” said James Felman, the Tampa defense attorney who is chair of the American Bar Association’s Sentencing Committee. “If they committed them today, they never would have seen the light of day. The only way they would have left jail was in a box.”

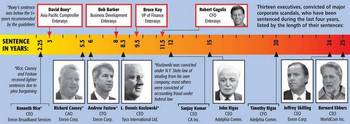

As it is, the former chief financial officer, Robert Gagalis, was sentenced to 11-1/2 years. The ex-vice president of finance at Enterasys, Bruce Kay, was sentenced to 9-1/2 years. And Robert Barber, of the company’s business development team, will spend eight years in prison.

They won’t get much time off for good behavior, either. Federal law requires them to serve 85 percent of their sentence before they are eligible for parole.

Narrower fraud

Their crime? The jury found them guilty of using accounting tricks to manipulate revenue, primarily in a crucial quarter ending Aug. 31, 2001, when Enterasys was spinning off from the Rochester-based Cabletron Systems — so that the new company would be able to meet Wall Street’s expectations.

The court eventually ruled that the fraud was responsible for $97 million of that loss.

Cabletron was once the largest employer in New Hampshire, but it had declined even before the spin off, and certainly was never in the same league as an Enron or WorldCom. The fraud involved was much more narrowly defined.

And while Enterasys never really recovered, and wound up being sold to private investors at a fraction of its value in 2001 – it never went bankrupt, and is still operating in Andover, Mass.

Yet the former Enterasys executives faced the same hefty sentences as the WorldCom and Enron executives. Indeed, the sentences they bargained for would have been the same faced by someone who robbed a bank and shot a teller, wounding, but not killing, him or her.

But by foregoing appeal, they avoided the possibility of even tougher sentences under the newer advisory sentencing guidelines, which were passed by Congress in response to the wave of corporate scandals in the 1990s.

Those new guidelines went into effect Nov. 1, 2001, and Barbadoro ruled that the conspiracy ended before that day, even though the executives filed inflated revenue figures with the Securities and Exchange Commission afterwards as well. Barbadoro also ruled that the defendants conspired to inflate revenue in 2002, but he said that was a separate conspiracy.

Even tougher guidelines

Deciding on sentencing guidelines was such a close call that Barbadoro – thinking that there was a good chance his decision would be overturned on appeal – he said he was prepared to sentence the executives under both guidelines.

The first sentence he meted out showed what a difference that would have made.

Barbadoro started with David Boey, comptroller of Enterasys’ Asia-Pacific division and clearly the lowest-ranking defendant on trial. Boey altered documents on a $3.5 million deal, following the instructions of some of those who testified against him.

Under the old guidelines, Boey faced a minimum of five years, and that didn’t include extra time for committing fraud outside the United States.

But Barbadoro agreed with Boey’s attorney’s assessment that he was an “order-taker, not an order-giver.” He also was sympathetic to Boey’s situation, which, as a foreign national, meant he faced near-certain deportation after serving his sentence, leaving behind the wife and children he worked so hard to bring to the United States.

So Barbadoro took two years off of the minimum guidelines, leaving Boey with a three-year sentence.

Under the new guidelines, even with the two years of forgiveness, Boey would have been sentenced to 11 years in prison.

At the time of Boey’s sentencing, Barbadoro made it clear that those executives higher up the chain of command would be facing much heavier penalties under both guidelines, and they didn’t wait around to find out what they were.

Barber struck his deal for an eight-year term – the lowest possible under the old guidelines — because he was concerned about the possibility of being sentenced under the more stringent guidelines.

“I weighed the benefits and the risks,” Barber told the court, “and I think this is a satisfactory arrangement.”

Barber was convicted for setting up “three-corner” deals, in which Enterasys used “investments” in shaky companies as a way to buy its own product through a distributor.

Kay and Gagalis were involved in both the three-corner deals and in recognizing the revenue from the Asia-Pacific deal. They also were convicted of knowingly filing false documents to the SEC.

Both were aware they would have faced even higher sentences than Barber under the old guidelines, and possibly even tougher sentences if they lost on appeal. In addition, like Barber, they also could receive a recommendation to serve their time in a prison with less violent offenders.

Even under newer November 2001 guidelines, the executives would have fared better than they would if their crimes had been committed after January 2003, when even tougher sentencing requirements went into place.

Under the 2003 guidelines, based on a loss determined at $97 million, Gagalis would face life without parole, said Felman.

“With those amendments [to the sentencing law] the consequences of a case like this one is truly frightening. Personally, I think the current guidelines are out of whack,” he said. “Duping documents to make your company look good, keep your salary and increase the value of your stock options is qualitatively different than stealing stockholders’ money to put in your pocket,” he said.

That’s what former Tyco International CEO L. Dennis Kozlowski and former CFO Mark Swartz were convicted of doing. Yet they were sentenced to 8-1/3 years in prison — a shorter term than both Kay and Gagalis — although they were convicted under New York law.

Considering all of this, Felman said that it was “smart lawyering” for attorneys to strike a deal, which he said was “very unusual” after the defendants were already convicted in trial.

Indeed, Barbadoro said he had never before approved such a settlement after a trial, “though I can understand why they did it.”