NHBR About Town: Week of June 19, 2026

Business and event happenings around the state of NH

Losing his Claremont home to foreclosure was almost the least of John Grossi’s problems. Last year, the 51-year-old machine shop quality control engineer said he had heart and brain surgery while trying to caring for a wife dying of bone cancer, one son was in trouble with the law, and his dad was paralyzed in another operation.

“It was one blow after another,” he said. “I hung onto the house as long as I could, but I couldn’t keep it up.”

He moved out in October, and CitiFinancial took back the title in a January foreclosure sale for $80,000. Now Grossi is struggling to pay the monthly rent on a two-bedroom apartment with his Social Security disability income while devoting most of his attention to his 14-year-old son, who still lives at home.

“It’s like Hiroshima after the blast,” he said. “I’m picking through the rubble of my life, trying to salvage something.”

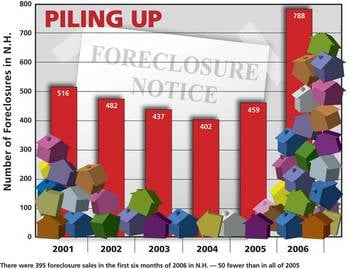

Grossi’s was one of 394 other foreclosure sales in the first six months of this year in New Hampshire, just 50 fewer than in all of 2005. While most probably aren’t as overwhelming as Grossi’s, each foreclosure is accompanied by a tale of woe and nearly all result in the loss of the borrower’s hard-earned equity. And nearly all of the former homeowners go on to pick through the rubble of their life’s dream in one way or another.

“It’s just sad, it’s just incredibly sad,” said Candace Gebhart, a paralegal with New Hampshire Legal Assistance who represents clients trying to hang on to their homes. Her caseload has more than doubled from last year.

Exactly why there is a sudden increase in mortgage foreclosures remains an open question. The number of foreclosure sales, which come from a database supplied by RealData based on actual Registry of Deed filings, actually dropped from its height in the mid-1990s, in the aftermath of the real estate depression.

But since 2003, the number of foreclosures has gradually increased, until shooting up this year – although the number is still less than half tallied during the mid-‘90s.

Creative financing

ForeclosuresMass.com also reports a sharp rise in property foreclosure in Massachusetts, and anecdotal reports at a recent conference focusing on foreclosure prevention noticed a similar spike was being experienced in the Midwest.

The Mortgage Bankers Association reports an increase in the foreclosure inventory rate from the first quarter of this year from the first quarter of last year, but not a spike.

MBA senior economist Mike Fratontoni said he was surprised the rate wasn’t even higher, given the recent 4.25 percent rise in interest rates and the hot refinancing market three or four years ago, which simply meant there were a lot more loans made to foreclose on later. The expected sharp rise in foreclosures, he said, has been offset by a strong economy.

However, first in the Midwest and now in the New England, that economy is cooling off.

“We have a perfect storm,” said Jeremy Shapiro, president of ForeclosuresMass.com (and ForeclosuresNH.com, which started last year). “We have rising interest rates, a number of creative loans written over the past years and a sharp appreciation and then a cooling off of the housing market.”

Heating prices over the past winter didn’t help. “All those who barely could make it under creative financing on what they had are unable to pay when the rates go up,” Shapiro said.

By creative financing, Shapiro is referring to a number of easy financing gimmicks, especially those loans offered to subprime borrowers — people with a checkered credit history. Because of the higher rates on the back end of many of those mortgages, and rather hefty fees tucked into the loan amount, underwriting standards aren’t as stringent.

“People with poor credit now have access to the mortgage market,” said Michael Collins, an Ithaca, N.Y., foreclosure consultant. “You might say this is a good thing: the democratization of home ownership. On the other hand, those with declining income or no income have to stretch further and further.”

That’s why it’s no surprise that the foreclosure rate among subprime lenders is nearly 10 times the rate of foreclosure on prime borrowers. In New Hampshire, a look at foreclosure data from the past 2-1/2 years shows that most foreclosed loans were originated by subprime lenders, with Ameriquest the leader of the pack (see sidebar).

Almost all subprime loans involve an adjustable-rate mortgage, so when interest rates stayed low, borrowers were able to survive that jump. Or if they couldn’t, they could always refinance with another sweet deal, though going deeper and deeper in debt in the process. Since prices appreciated, there seemed to be always more equity available to borrow from.

But equity can’t stretch for ever. As housing prices leveled off – and in some cases declined – the borrowers found that they owed more than they owned. There was simply no more equity left to back another loan.

“When you are upside-down like that, there are very few options to avoid foreclosure,” said Shapiro.

Get in touch

Even those who have filed for bankruptcy are having trouble hanging onto to their homes.

Peter Wright, who heads the consumer clinic at the Franklin Pierce Law Center in Concord, said that a number of his Chapter 13 clients couldn’t keep up on payment arrangements after bankruptcy filings. He also thinks that fewer people can file for bankruptcy these days because the new bankruptcy law has driven some attorneys out of the field. Without a lawyer to work out a Chapter 13 stay, there is one less tool to prevent someone from losing his or her home.

Thus all experts agree: Borrowers should get in touch with their lender before it comes to that. But many of those who fall behind in their payments stick their head in the sand. A survey conducted by Collins showed that a large percentage of borrowers think that discussing their problem with their lender might spur the lender to foreclose. The reverse is true.

“The earlier the better — as soon as you know you are going to be in trouble,” said Phillip Gioeli, a borrower’s assistant in the loss mitigation department of Option One, one of the largest subprime lenders.

The foreclosure process is an expensive one, and lenders tend to lose money on the deal. (For those who want some third-party intervention, they can call 888-955-HOPE, or visit hpfonline.com.)

If worse came to worst, Gioeli said, the borrower could deed back the property to the mortgage holder. While the borrower would lose the equity put into the house, at least the foreclosure fees wouldn’t be added to the debt. As part of the deal, the mortgage holder might be able give back some equity to the borrower if he or she managed to sell the property more then the debt.

“Might” is the operative word. Most loans are sold by the originators to various investors. Sometimes these investors are big institutions that have their own mitigation loss department. In the case of federally backed prime loans, the noteholders also have various government guidelines and restrictions that tend to protect the borrower.

In the subprime world, however, such “nonconforming” loans are often sold to smaller investors, and there is often no federally backing involved.

Meanwhile services like ForeclosuresNH.com are helping to create an alternative foreclosure market. For a fee, the service lets investors know when a property is in foreclosure. That’s the time to approach the owner — not when the title is taken by the bank, said Shapiro.

“After the deal goes to auction, the bank tries to recover all of the foreclosure costs and puts it on for market value. Tell me, where is the deal? The sooner you can get in there, the more equity there is to go around,” he said.

Business and event happenings around the state of NH

The Latest is a roundup of the comings and goings of the movers and shakers in NH's business community

A brand new and redesigned Revo Casino and Social House came back to Manchester’s land-use boards this month after the acquisition of additional nearby properties allowed the creation of an expanded vision for the project.

The New Hampshire House and Senate sent three bills to Gov. Kelly Ayotte intended to enable more housing construction, overcoming opposition from the New Hampshire Municipal Association and others.

HEALTH CARE By: DR. STEVEN ANGELO As more Americans live longer, maintaining brain health is becoming an increasingly important part of overall well-being. During Alzheimer’s & Brain Awareness Month, and throughout the year,…

Small and medium-sized enterprises (SMEs) make up the majority of businesses in NH and play a vital role in driving economic growth, innovation and job creation.

Keene’s downtown infrastructure project will tentatively break ground in Central Square on July 6, Keene’s public work director said last Wednesday.

Successful investing takes a lot of patience. Risk tolerance and time horizon are important factors in determining an appropriate investment strategy. For example, some investments would be unwise to choose if the principal is…

From left, former Yankee Publishing CEO Jamie Trowbridge; Granite VNA President and CEO Beth Slepian; CASA New Hampshire President and CEO Marty Sink; President and CEO of the Palace Theatre Trust Peter Ramsey; and President and…