New state law empowers homeowners with ‘balcony’ solar panels

With a new state law set to go into effect with the dawn of a new year in 2027, Granite Staters will be able to install so-called “balcony solar” panels for home use.

As the dust settles on the Affordable Care Act, New Hampshire is feeling tremors from shifts occurring nationally, although the state’s health care landscape is more stable than the rest of the country.

About a quarter of the nation, geographically, and around 17 percent, demographically, only have one insurer on the exchange, meaning less competition on rates, and therefore higher costs. Over the past year, UnitedHealthcare, Aetna and Humana have pulled out of the markets in most states, not getting the healthy populations they expected.

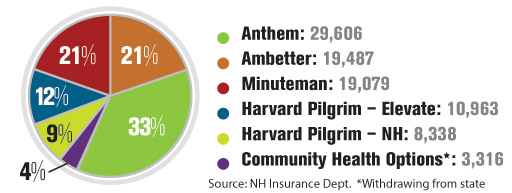

While New Hampshire has lost one insurer on the exchange – Community Health Options – the four largest are left standing. Costs may go up in the individual market more than in the last few years – about an 11 percent increase – but less than half of rates proposed in the rest of the country, according to one analysis. And rate increases in the group market will be smaller. There have also been some creative solutions, increasing alliances between providers and insurers and the advent of telemedicine.

However, there are challenges ahead as the federal government diminishes funding for expanded Medicaid and transitional payments to insurers.

Managing Medicaid

The current national landscape is where New Hampshire was in 2014, when the exchange first started. Back then, Anthem Blue Cross and Blue Shield of New Hampshire was the only insurer in the state offering coverage on the exchange.

But, as Jenny Patterson, health policy legal counsel at the New Hampshire Insurance Department put it, “New Hampshire has gone in the opposite direction.”

That’s partly because New Hampshire forged its own path with expanded Medicaid, delivering an uninsured population – which surpassed 50,000 last month – to the private insurance market rather than adding them to the Medicaid rolls.

Last year, the state continued federal funding for the program by meeting the state’s five percent match without spending a penny of taxpayer money, instead getting providers and hospitals to cough it up. But the state’s share will go up next year, and double by 2019, so it’s not clear whether state lawmakers will have the political will to chip in or if providers and hospitals can continue to bear the cost.

Half of this Medicaid-eligible population – about 20,000 people at the time – went to Ambetter, a product of Centene Corporation, which already had most of that population under the Medicaid managed care contract. But the rest, which has since grown to about 30,000, were split up among the other carriers.

Straining carriers

But this provided a strain on some carriers, particularly on Maine-based Community Health Options, which said it underestimated the cost of taking on the new Medicaid patients. CHO lost $73 million in 2015, the year it entered the state, and $12 million in the first half of 2016.

CHO, New Hampshire’s smallest insurer on the exchange, peaked at about 9,200 individuals in March, but about 30 percent were expanded Medicaid recipients. The company simply couldn’t put up with the pent-up demand. It stopped writing new policies, and in September it agreed with the state Insurance Department to withdraw from the state, meaning that 3,000 remaining individuals and the 8,000 people covered through its group programs had to be switched to another insurer. (CHO did not return calls to NH Business Review.)

Increasing costs and changing networks

CHO’s exit leaves a few holes in the state insurance market. It was the only company to offer a preferred provider organization (PPO), a vanishing option particularly under the ACA where narrower networks are the rule. PPOs make it easier for patients with special health needs, such as cancer or rare childhood diseases, to more easily access high specialized providers out of state.

Ray White, president of Cornerstone Benefit and Retirement Group, Inc. in Bedford, sees them as the successor for those that used to be under the expensive assigned risk pool, that ended when the ACA required insurers to take all comers – pre-existing conditions or not.

“Now there will be no plan for sale [on the individual exchange] with a network that allows you to go down to Boston,” he said. “It’s the first time these people have nowhere else to go.”

CHO also had more than 90 percent of the 825 businesses on the SHOP exchange that covered about 7,615 employees. SHOP offered two years of generous tax credits for some small businesses, particularly those with moderate income employees, and also offered an added benefit – which only started working earlier this year – of allowing employees to pick their own policy online, much like individuals do on the exchange. Now, aside from the 39 still being serviced by CHO, there are only 110 businesses.

“SHOP was stillborn,” said White.

Another disappointment has been that Ambetter – which also did not respond to calls – appears to be content with its expanded Medicaid population. The company has filed one rate filing with the state insurance department.

“They are just parking their plan and not doing the marketing,” White said.

The good news is that Ambetter’s proposed increase, 1.35 percent, is the lowest of any carrier. That might spark more interest than any marketing campaign.

The other three carriers are competing both on price and on network offerings on the exchange. At deadline, all but two hospitals are on more than one network, and all but three hospitals are on more than two networks.

Proposed changes to individual rates average 11 percent, less than half of those proposed in the rest of the country, according to one analysis, but both figures could be misleading. As noted by White, New England had higher rates to begin with, so this could mean that the rest of the country is just catching up.

Secondly, an analysis of approved rates in selected states show actual rates going up about 9 percent. And New Hampshire numbers included sharp increases by CHO and Minuteman, which indicated that the approved rates will be a lot lower.

Anthem Blue Cross Blue Shield is still the state’s largest carrier, with about a third of the nearly 91,000 individuals on the exchange. Once criticized when it was the only carrier in 2014 for introducing its narrow network, it now covers all but four hospitals, according to the state Insurance Department’s website.

In June, Anthem proposed rate increases ranging from 5.5 to 9.5 percent, though New Hampshire President Lisa Guertin said the approved rates might come in just past the double-digit mark.

Guertin said she is “pleased” that prices have been relatively stable, and blames prescription drugs prices for some of the increases this year. The other has been the phasing out of various federal transition payments, meant to compensate insurers for taking on higher risk patients.

To cope with some of these cost drivers and to approve care, Anthem is attempting to switch to a reimbursement system that rewards better health outcomes rather than volume, and the implementation of a telemedicine program that allows you to virtually visit a real doctor on a smartphone.

These are both concepts employed by Anthem’s largest competitor, Harvard Pilgrim, which has more than 19,000 individuals on the exchange and 8,300 on its broad network that includes all the hospitals and just short of 1,100 in its narrower network that includes 16 hospitals.

Harvard Pilgrim proposed rate filings for individuals were between 4.3 and 6.6 percent. The filing for its groups – which cover about 75,000 – were not available. But the company said that the weighted average would be about 11.1 percent.

Harvard Pilgrim also blames drug prices, which have gone so high that it surpassed inpatient costs among certain groups. The company also increased some benefits. Those on the cheaper bronze plan, for example, will get four non-preventive visits before deductibles kick in. Harvard Pilgrim also has a “Doctor on Demand” program that can be accessed with a smartphone.

Harvard Pilgrim also offers Benevera Health – a collaborative venture that includes Dartmouth-Hitchcock, Elliot Health System, Frisbie Memorial Hospital and St. Joseph Hospital in Nashua last April – as an added service for those off and on the exchange.

Instead of managing the care of those who are already chronically ill, “we can predict with amazing accuracy which people are at high risk,” said Dr. William Brewster, vice president of New Hampshire Regional Market at Harvard Pilgrim Health Care.

The third major carrier, Minuteman Health, another co-op, based in Massachusetts, has about 19,000 members on the exchange, with only 15 hospitals. It had filed among the steepest rate increases ranging from 18 to 60 percent in June. But the company now says that weight average will be closer to seven percent (which includes its lower-priced group rates).

That’s because of all the uncertainty involving risk assessment. Risk assessment – not to be confused by risk corridor – is what insurers with healthier populations pay insurers with sicker populations. Minuteman is in a fierce legal battle over how much it owes the federal government under risk assessment, arguing that the current formula penalizes the insurer for keeping premiums down and growing quickly. Minuteman did manage to get the last assessment decreased by $1 million to $16.7 million, and said that its initial estimation for the next one was too high – thus the downsizing of rates.

Unlike many co-ops, it reported a small ($226,000) profit year-to-date, which was better than the first half of 2015, when it lost $8.5 million. Minuteman doesn’t apologize for its narrow network. Indeed, it credits it for keeping costs down.

“We have a traditional narrow network,” said Minuteman’s Keith Ledoux, vice president of sales & retention. “We negotiated with providers and if they are not willing to come to terms, we walk away.”

With a new state law set to go into effect with the dawn of a new year in 2027, Granite Staters will be able to install so-called “balcony solar” panels for home use.

Marmon Utility President Ken Woo highlights how the company has been delivering electric infrastructure supports for 75 years

Gather’s new culinary education program, Fresh Start, is a way to teach people with employment challenges the kitchen skills and life skills they need to have a career in the food service industry

Artificial intelligence is transforming business at remarkable speed. Most discussions focus on productivity gains, cost savings or the jobs AI may eventually replace. Yet a more significant change is already underway — one that could reshape the future of nearly every profession.

Good news for patients — and a reminder of what’s at stake

New Hampshire businesses are facing a workforce challenge that goes beyond wages and hiring.

5 tips for creating an estate plan that reflects all of your legacy

Business and event happenings around the state of NH

The Latest is a roundup of the comings and goings of the movers and shakers in NH's business community