Ever since the Affordable Care Act became law, the focus has been on the market for individual consumers. That’s where a lot of the action is, so that is where the media spotlight is.

But it isn’t where most of the people who have health insurance are.

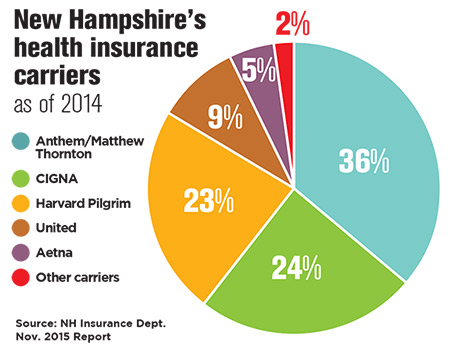

Even though nearly 90,000 individuals have signed up for the ACA public exchange in New Hampshire, four out of five people are in some kind of group plan. Anthem Blue Cross Blue Shield, for instance, covers 228,000 individuals in group plans, Harvard-Pilgrim Health Care covers another 80,000 in group plans, and Tufts Health Freedom Plan – the new kid on the block – covers 18,000. And that doesn’t include the number of individuals covered under plans issued by larger national insurers like Aetna and Cigna, which cater to larger employers. Nor does it count those enrolled in businesses that are self-insured.

For the coming year, there is some good news in that proposed increases in small group rates in New Hampshire seem to be in the low single-digits, while filings on the individual exchange are more than 10 percent. Still, changes are happening in the group market, and not all of them are good.

Grandmother and grandfather

“If you like the plan you have, you can keep it.” These oft-quoted words of President Barack Obama were not true before the ACA passed, and they aren’t true today.

Before the law was enacted, it wasn’t true for employees, whose coverage depended on the choices made by their employers. And it wasn’t true of businesses, which had to consistently adjust their plans to keep costs down and their workers happy.

However, some groups have been able to keep their exact same plan. These groups cover more than 20,000 individuals, according to Anthem, which has most of the legacy plans.

About 10,000 of those people are in plans that were “grandfathered” before March 23, 2010, the date of the ACA’s enactment. But groups are discovering that legacy plans are no longer grandfathered because they have been changed enough to lose their status, said Steve Gerlach, an attorney with the law firm of Bernstein Shur and an expert on the ACA.

“I think they will all fade into the sunset in a few years,” he said of those grandfathered plans.

However, so-called “grandmothered” plans – in effect after the ACA’s enactment but before the exchanges started in 2014 – won’t sunset, but they will have to be upgraded at the end of 2017.

Freedom Energy Logistics, an energy consultancy and management firm in Auburn, has one of those grandmothered plans. The company pays 95 percent of the premium covering its 19 employees, even though it costs a bit more at times because it offers better coverage, said Chief Operating Officer Bart Fromuth, who also is a Republican state representative from Bedford. This year, it was actually cheaper than other plans.

“We value our employees, and we want to remain competitive with a higher-quality plan,” he said.

List vs. composite billing

What concerned Fromuth most about conforming to the ACA was list billing.

Before the law, insurers presented one bill for all employees, and the employer decided how much to contribute. Everybody paid the same. But after 2014, insurers billed for each employee separately, showing how much each employee costs to insure. If the company wanted everyone to pay the same, they would pay more for older, sicker workers.

But some insurers are moving away from list billing. Minuteman Health, for instance, argued that the law only requires that it be offered, so it is switching to composite billing, which it says will allow it to be more competitive in the group market. Thus far, the Massachusetts-based insurer has focused primarily on the individual exchange in New Hampshire, but it does cover more than 400 people through group plans.

Employer penalty

Another major change coming down the pike – a hefty tax on so-called “Cadillac plans” that offer generous coverage – was also supposed to go into effect in 2018, but was pushed back again for two years.

However, the employer penalty (employer shared responsibility payments) went into effect starting in 2015 for firms with more than 100 or more full-time equivalents that don’t insure 70 percent of their full-time workforce, and this year it ratcheted down to firms with 50 or more FTEs that don’t insure 95 percent of their workers.

These provisions come with extremely complicated monthly tax forms that had to be filed last year, but most accountants and benefit companies have already adopted to it.

“It was turbulent at first, but the first round was approved by the IRS,” said Josh Robinson, president of Checkmate Workforce Management Solutions, which developed a software tool to handle the ACA requirements. “There is a lot less chatter about that among my clients. It is part of the business process.”

Now some of the larger firms that filed in April are starting to hear back from the IRS.

That’s because the law is triggered when an employee signs up for coverage on the exchange. To get a subsidy, people must identify their current employer as not offering affordable coverage. The exact amount of the subsidy they are entitled to is not revealed until they enter their tax information into a software program or give it to an accountant.

The IRS, armed with this information, is starting to send notices out to the companies identified.

“We are starting to see the beginning of enforcement,” said Gerlach.

So far, less than 5 percent of his clients have received a notice, and a large percentage of those are the result of errors, since many actually had been offering affordable coverage. An employer has the right to appeal as well, and eventually the IRS will have to determine who has to pay up – the employer or the employee.

Employers aren’t the only ones that have to pay. Insurers have to send out refunds to their customers if they spend less than 80 percent on individual and small group medical care, and 85 percent for large group, by Aug. 1. Statistics for 2015 aren’t in yet, but in 2014, insurers refunded $469 million nationally, and $9 million in New Hampshire. Nationwide, the refunds were split in half between groups and individuals, but in New Hampshire almost all the refunds went to 54,500 individuals, about $197 a person – nearly $40 above the national average. No small group insurers had to pay a penalty, but large group insurers paid $133,000. That money was refunded to about 281 customers, with an average refund of $945, or nine times the national average.

Systematic changes

There also has been some more systematic change caused by transforming a traditional fee-for-service health care system to a data-driven, transparent, outcomes-based system. If this new payment system rewards providers for keeping people out of hospitals rather than filling the beds, what do you do with all the empty beds and the staff that served them?

Hospital margins are now down to 1 percent in the Granite State, said Steve Ahnen, president of the NH Hospital Association, half of what it was when the ACA was enacted.

The “headwinds” eased off in the past few years, he said, but thanks to the high cost of drugs and the high median age of state residents, they are picking up again.

Hospitals have tried to deal with this though various alliances, partnering with larger medical providers down in Massachusetts or teaming up with insurance companies. Harvard Pilgrim set up Benevera Health, a partnership with four New Hampshire hospitals (Dartmouth-Hitchcock, Elliot, Frisbie Memorial and St. Joseph) in an attempt to drive down costs. And Tufts has joined with five systems (Catholic Medical Center, Concord Hospital, LRGHealthcare, Southern New Hampshire and Wentworth-Douglass) to create the Granite Healthcare Network. It also has struck a deal with Northeast Delta Dental.

Despite such efforts, Dartmouth Hitchcock ended up its 2016 fiscal year with a $12 million deficit and announced plans to reduce its staff by as much as 5 percent, though the exact number of layoffs won’t be announced until Oct. 17.

All sides are turning to technology in the hopes of lowering cost. Both Anthem and Harvard Pilgrim now reimburse for telemedicine consultations, enabling doctors to treat patients in rural areas and consult with experts in Boston.

In addition, employers are starting to look at utilizing private exchanges. Instead of a government subsidy offered on public exchanges, the company gives employees a defined contribution and offers them an array of plans, and they pick how much of their own money they want to spend. Some large employers have offered this in the past, but only in the last few years third parties started offering them to smaller employers, encouraged by evolving technology.

On private exchanges, “employers have more control of their budget and employees have more choice of what they are shopping for,” said Gerlach.

Private exchanges allow employers to offer very generous benefits – fulfilling the requirements of the ACA – while letting employees choose the lower-cost ones, which they tend to do. They also allow employees to purchase a number of other products, including dental coverage.

Nationally, private exchanges covered 6 million people in 2015, double the previous year, but their growth slackened off a bit because the threat of that Cadillac tax has been pushed off.

New Hampshire, in particular, has lagged behind the rest of the nation when it comes to private exchanges, according to Tom Whitty, of Liazon Corp., a Buffalo, N.Y.-based company that has been working with Maine-based Cross Insurance, among others, to offer such exchanges.

Thus far, fewer than 10 companies have signed up in New Hampshire, but Whitty said he expects the recent addition of the Harvard Pilgrim provider network on Liazon exchanges will make it more attractive.

Likewise, the Business and Industry Association of NH is working with Anthem to offer a private exchange for its members, and although “there are lots and lots of tire-kickers” no one has signed up yet, said BIA spokesman Kevin Flynn. But Flynn said he thinks it is because it wasn’t out in time for open enrollment last year. The true test is this time around.

“It’s a brave new world for health insurance,” said Flynn.