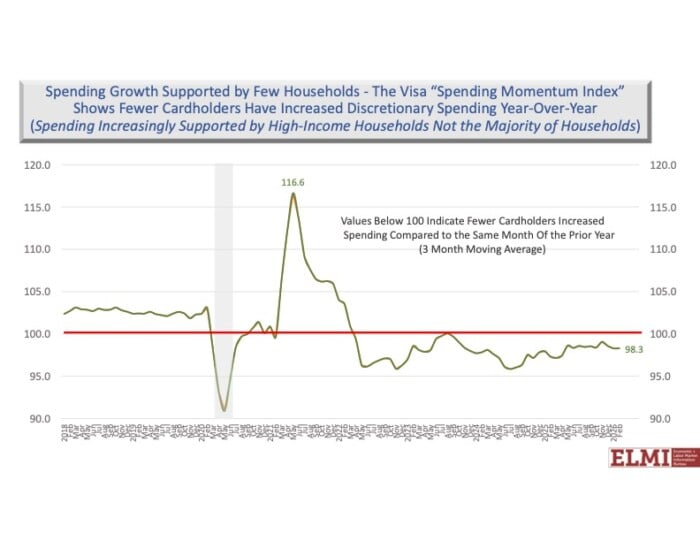

NH economist lowers forecast for 2026

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

Achieving financial independence — that is, living comfortably while knowing your money will last — is a goal shared by many. Taxes influence nearly every financial decision, and understanding the impact of these changes is key to optimizing your plan.

Here are six areas to review with your tax advisor:

1. Increased State and Local Tax (SALT) Deduction

The SALT deduction allows taxpayers to deduct certain state and local taxes from federal taxable income. Previously capped at $10,000, the deduction increases to $40,000 starting in 2025 and will rise by 1% annually through 2029 before reverting to $10,000 in 2030.

For individuals with a modified adjusted gross income (MAGI) between $500,000 and $600,000, the increased SALT deduction gradually decreases. Those with an income above $600,000 remain subject to the $10,000 cap. This change is especially relevant for taxpayers in states with high property or income taxes.

If you fall into this category, the increased SALT deduction could lower your federal tax bill.

2. Enhanced Deduction for Seniors

From 2025 to 2028, taxpayers aged 65 and older can claim an additional $6,000 deduction per person ($12,000 for married couples filing jointly).

Income limitations apply. The phase-out begins at $150,000 MAGI for those Married Filing Jointly (phased out completely at $250,000 MAGI for MFJ), or $75,000 MAGI for all other taxpayer filing statuses (phased out completely at $175,000 MAGI for a single filer).

This new deduction may help offset taxes on Social Security benefits and improve retirement cash flow, offering seniors a meaningful opportunity to reduce their tax burden during retirement.

3. Roth Conversions & Stable Tax Brackets

With the passing of the One Big Beautiful Bill in July 2025, federal income tax brackets will remain unchanged going into 2026.

This stability is especially helpful when considering Roth conversions, which involve transferring funds from a pre-tax retirement account to a post-tax Roth IRA and paying taxes on the converted amount.

If you expect to be in a higher tax bracket in retirement, perhaps due to required minimum distributions (RMDs), converting some of your pre-tax assets now may reduce future tax liability.

With more certainty around tax rates, you and your tax advisor can better evaluate whether a Roth conversion could benefit you.

4. Tax-Advantaged Savings for Families (Newborn Accounts & 529 Plan Expansion)

Two new provisions make it easier for families to save for their children’s futures.

First, children born between 2025 and 2028 are eligible for a one-time $1,000 deposit from the federal government into a newborn savings account. Families can contribute up to $5,000 annually until the child turns 18, with employer contributions counting toward this limit. Qualified distributions can begin once the child reaches age 18 and are taxed only on earnings at long-term capital gains rates.

Second, 529 plans cover a broader range of K-12 expenses, including curriculum, books, tutoring and therapies for students with disabilities. The aggregate limit of these deductions will increase from $10,000 in 2025, to $20,000 in 2026.

5. Charitable Deductions

Beginning in 2026, taxpayers who itemize will only be able to deduct the portion of charitable giving that exceeds 0.5% of adjusted gross income (AGI). Previous AGI limits remain unchanged.

Those who do not itemize will be eligible to deduct up to $1,000 annually ($2,000 for married couples filing jointly) for qualified charitable contributions, which may help reduce overall tax liability.

If you’re considering charitable giving, you may want to discuss with a tax advisor whether it’s beneficial to make additional charitable contributions before the new 0.5% AGI floor takes effect.

6. Section 199A: Deduction for Qualified Small Business Income

The Qualified Business Income (QBI) deduction, originally introduced in 2017, allows eligible small business owners to deduct up to 20% of income from qualified business activity.

The deduction will remain at 20%, with phase-outs beginning at $75,000 for single filers and $150,000 for married couples filing jointly.

Small business owners can continue to benefit from this deduction, potentially lowering tax liability and improving cash flows.

The long-term success of your financial plan can be heavily influenced by the types and amounts of taxes paid. To this end, take the time to discuss these topics with your tax advisor to better understand your options before taking any action.

William J. Fleming is vice president, manager of financial planning, with Cambridge Trust Wealth Management, a Division of Eastern Bank, based in Manchester, NH.

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

If nothing changes between now and then, the trust fund that finances Social Security payments will run out, triggering a 7% decline in monthly payments in 2032 and dwindling further to 28% from 2033 through 2036.

Our post-pandemic business environment has brought about myriad challenges that make cash flow forecasting much more difficult than it was five years ago. Many businesses are navigating supply chain challenges, volatile demand and lingering inflation — all key indicators of future cash flow.

Howard Brodsky, co-founder and chairman of CCA Global Partners (CCA), highlighted the power of cooperatives (co-ops) — shared business models owned and governed by their members — as the “great economic equalizer” for small businesses worldwide in his remarks at the United Nation’s (UN) annual Session of the Commission for Social Development at UN headquarters in New York City. This session convened global business leaders and innovators to discuss advancing social development and social justice through coordinated, equitable and inclusive policies.

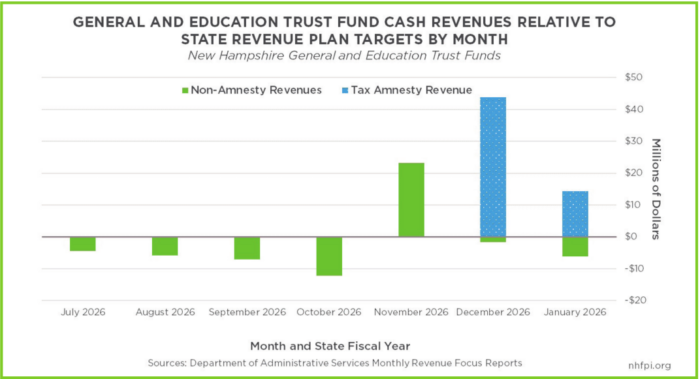

Analysts fear overall revenue will lag unless other accounts pick up the pace

Analysts fear that once it’s gone for the remainder of the fiscal year, overall revenue will lag unless other accounts, which have been underperforming to date, pick up the pace

A judge has dismissed a lawsuit filed by more than 70 Hampton taxpayers who argued the town’s 2024 revaluation — which led to increased tax bills — was conducted unfairly and unlawfully.

Making deposits at local banks means more money being reinvested in your community

There are no magic wands in tax disputes, but the current New Hampshire Department of Revenue Administration (DRA) tax amnesty program is about as close as it gets.