NH economist lowers forecast for 2026

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

Retirement is one of the most important financial goals for many married couples. It’s something you may dream about and work hard to reach. But, even if you feel like you are on track in terms of meeting your financial objectives, there is an equally important factor to consider: Are you both on the same page about your vision and plans for retirement?

Retirement is one of the most important financial goals for many married couples. It’s something you may dream about and work hard to reach. But, even if you feel like you are on track in terms of meeting your financial objectives, there is an equally important factor to consider: Are you both on the same page about your vision and plans for retirement?

For example, what if your ideal experience in retirement is to travel, but your spouse is looking to stay local to be near family. Have conversations in advance of retirement to make sure you and your spouse are on the same page.

The years leading up to retirement are an important time to compare their ideas and see if there are any obvious conflicts. Among the different topics to address:

Don’t be alarmed if you and your spouse don’t have the exact same idea of how retirement should work for you. It isn’t unusual. What’s important is finding ways to come to an agreement. That may mean each side has to give a little to make it work.

Flexibility is also key. Once the reality of retirement sets in, either person’s viewpoint might change and that could affect your decisions. Be prepared for the potential that a medical event could alter your plans, as this is more likely to be a factor as you grow older. Your financial circumstances are also always a consideration. Have a discussion with your financial advisor about your retirement plans and try to have an agreed-upon strategy in place before you wrap up your working years.

Filling a retirement savings gap

Filling a retirement savings gap

Are you on track to achieve your retirement savings goals? It’s important to establish a target savings amount and regularly make retirement plan contributions. It’s also vital to regularly check your progress so you know if you are on the right track. Should you determine that you are falling behind on your savings goals, it’s time to try to rectify the situation.

Any or all of the following solutions can help you overcome a retirement savings gap:

Keeping up with rising healthcare costs

For most of us, the reality of growing older means that medical issues will likely become a more common concern. As a result, healthcare can become a prominent expense in retirement. Medicare typically serves as the foundation of your health insurance later in life, as it starts at age 65. If you retire prior to age 65, you’ll find insurance coverage to be expensive, with significant, potential out-of-pocket costs.

For most, healthcare expenses become greater as they grow older. According to statistics compiled by the Kaiser Family Foundation, annual health spending for the average woman is $11,694 for those ages 65 and up. This compares to average annual expenditures of $8,343 for those age 55-64, and $5,775 for women ages 45-54. Spending patterns are similar when comparing costs for those different age groups among men.

At the same time, changes in healthcare costs in general tend to outpace the standard rate of inflation. Rapidly rising healthcare costs can quickly eat away at your retirement savings as you age.

The reality is that while Medicare helps make health insurance much more affordable for older Americans, it is far from free. You will pay premiums for Medicare Part B (doctor’s visits and other care services). The premiums typically rise each year. If you choose Medicare Part D (prescription drug coverage), there is an additional premium, but that should be offset by lower drug costs. You may also choose to purchase a Medicare Supplemental Insurance plan that could add hundreds of dollars to your monthly budget but limit other out-of-pocket expenses.

Good planning can help you prepare for the challenges posed by medical costs in retirement. Potential steps to address this issue include:

Be sure to consult with your financial advisor to learn more about the potential financial challenges you face with healthcare in retirement and to explore steps you should take today.

Bob Bonfiglio is a private wealth advisor and managing director with Rise Private Wealth Management, a private wealth advisory practice of Ameriprise Financial Services Inc. in Bedford. He can be contacted at bobbonfiglio.com or by calling 603-606-4255.

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

If nothing changes between now and then, the trust fund that finances Social Security payments will run out, triggering a 7% decline in monthly payments in 2032 and dwindling further to 28% from 2033 through 2036.

Our post-pandemic business environment has brought about myriad challenges that make cash flow forecasting much more difficult than it was five years ago. Many businesses are navigating supply chain challenges, volatile demand and lingering inflation — all key indicators of future cash flow.

Howard Brodsky, co-founder and chairman of CCA Global Partners (CCA), highlighted the power of cooperatives (co-ops) — shared business models owned and governed by their members — as the “great economic equalizer” for small businesses worldwide in his remarks at the United Nation’s (UN) annual Session of the Commission for Social Development at UN headquarters in New York City. This session convened global business leaders and innovators to discuss advancing social development and social justice through coordinated, equitable and inclusive policies.

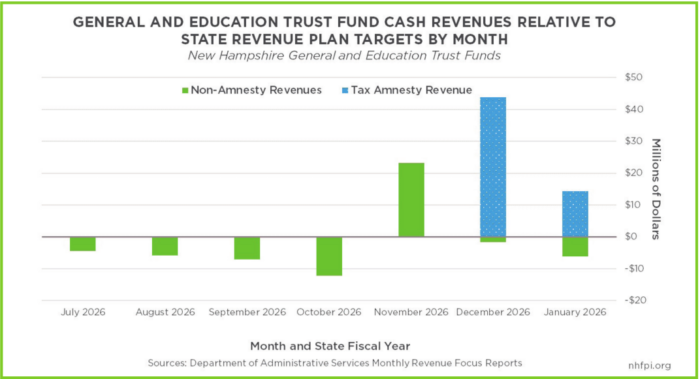

Analysts fear overall revenue will lag unless other accounts pick up the pace

Analysts fear that once it’s gone for the remainder of the fiscal year, overall revenue will lag unless other accounts, which have been underperforming to date, pick up the pace

A judge has dismissed a lawsuit filed by more than 70 Hampton taxpayers who argued the town’s 2024 revaluation — which led to increased tax bills — was conducted unfairly and unlawfully.

Making deposits at local banks means more money being reinvested in your community

There are no magic wands in tax disputes, but the current New Hampshire Department of Revenue Administration (DRA) tax amnesty program is about as close as it gets.