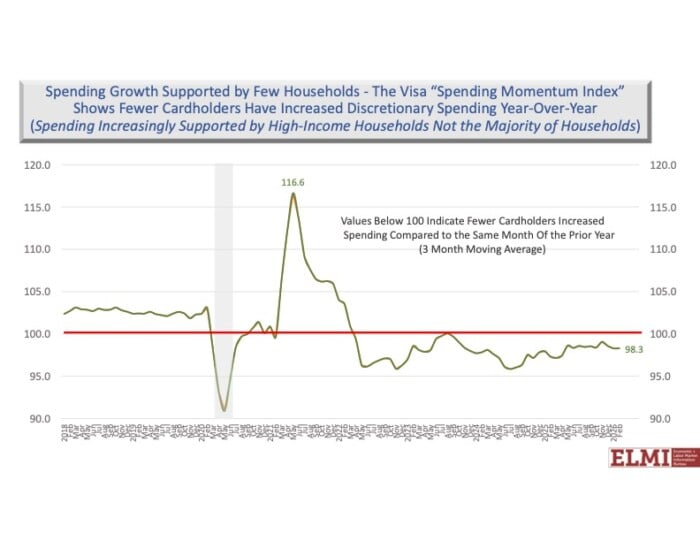

NH economist lowers forecast for 2026

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

Our post-pandemic business environment has brought about myriad challenges that make cash flow forecasting much more difficult than it was five years ago. Many businesses are navigating supply chain challenges, volatile demand and lingering inflation — all key indicators of future cash flow.

Unpredictable cash flow makes it extremely difficult for businesses to accurately plan for future investments, identify funding needs or optimize unexpected cash surpluses, and it can also lead to shortfalls resulting in missed payments, damaged vendor relationships and increased reliance on debt.

That’s where banks come in; bankers offer business clients a variety of tools to help manage inevitable cash flow surprises. Digital transaction data provides historical insights and predictive analysis tools, seasonal planning guidance can anticipate large swings in revenue or expenses, and lines of credit maintain a flexible safety net.

Getting ahead of cash flow surprises

Digital banking solutions and treasury management tools provide access to real-time cash flow data, historical cash inflows and outflows, and all transaction history. Treasury management tools and advisors can help a business optimize liquidity and adjust for uncertainty when appropriate.

Business owners should meet with their bank’s advisory team to review the data and forecasts using the bank’s digital tools and model various scenarios based on the business’s cycles, aiding decision-making and preparation for cash flow surpluses and shortfalls.

Using lines of credit to build a flexible safety net

Even with the best planning and forecasting, the unexpected can happen. Businesses should consider establishing a line of credit for short-term access to capital if cash gets tight. This will help manage unplanned expenses like a major repair, or a temporary cash flow gap. It is critical, however, to repay these funds as soon as possible to maintain ongoing liquidity and a strong financial profile.

Banks offer a variety of credit line options to provide businesses with access to that much-needed capital. A working capital line helps fill the gap between accounts receivable and accounts payable, support orders and contracts received, and may help build inventory during business cycle peaks. A business overdraft line provides protection for business checking accounts by covering charges in excess of your current balance. These credit line options are not meant to be used as a permanent solution, though. For longer-term credit needs, banks can consider providing multi-year credit arrangements tailored to the business profile and need. Pairing cash flow forecasting and credit usage helps businesses time withdrawals and payments wisely to ensure they have necessary, timely cash flow support.

Managing the highs and lows of seasonal businesses

By nature, seasonal businesses face cash flow highs and lows each year. Amusement parks, summer camps and golf courses, to name a few, are going to generate much more revenue in the warmer months compared with colder months, making cash flow forecasting and management that much more important. Rent payments, insurance, employee salaries and other general overhead bills must be paid year-round.

Seasonal businesses can utilize both cash flow forecasting and lines of credit, just as year-round businesses do, but they should also develop a lean, off-peak budget, set aside cash reserves from peak season, and look at ways to diversify revenue streams.

Seasonal businesses can minimize year-round costs by hiring seasonal employees, not overstocking inventory, and negotiating vendor contracts to extend payment terms or get discounts on bulk orders. The cash set aside from peak season covers fixed year-round expenses. To generate revenue during the off-season, some businesses may consider selling gift cards, discounted peak-season passes and other offers. Some businesses may even extend their season with different paid experiences — for instance, a golf course may offer cross-country skiing and snowshoeing, a ski resort may offer hiking, lift rides for leaf peeping or mountain biking, and a farm stand may offer hayrides.

No matter what your business may be, cash flow resilience is key to long-term success. In a volatile economic climate, having a trusted banking partner makes all the difference. At NBT Bank, our business and commercial banking team is here to help manage your business’s finances and achieve its goals.

Marilyn Charbonneau is senior business banking officer for NBT Bank.

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

If nothing changes between now and then, the trust fund that finances Social Security payments will run out, triggering a 7% decline in monthly payments in 2032 and dwindling further to 28% from 2033 through 2036.

Our post-pandemic business environment has brought about myriad challenges that make cash flow forecasting much more difficult than it was five years ago. Many businesses are navigating supply chain challenges, volatile demand and lingering inflation — all key indicators of future cash flow.

Howard Brodsky, co-founder and chairman of CCA Global Partners (CCA), highlighted the power of cooperatives (co-ops) — shared business models owned and governed by their members — as the “great economic equalizer” for small businesses worldwide in his remarks at the United Nation’s (UN) annual Session of the Commission for Social Development at UN headquarters in New York City. This session convened global business leaders and innovators to discuss advancing social development and social justice through coordinated, equitable and inclusive policies.

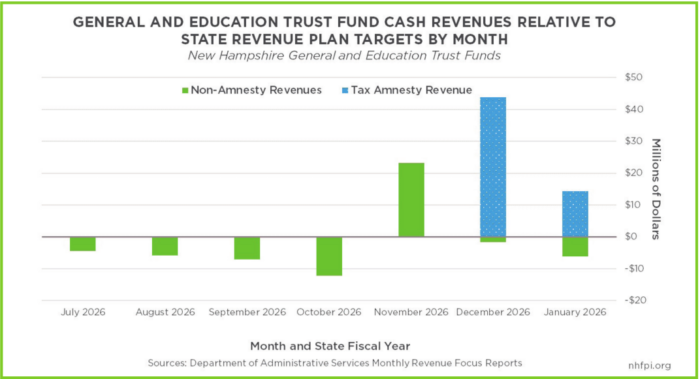

Analysts fear overall revenue will lag unless other accounts pick up the pace

Analysts fear that once it’s gone for the remainder of the fiscal year, overall revenue will lag unless other accounts, which have been underperforming to date, pick up the pace

A judge has dismissed a lawsuit filed by more than 70 Hampton taxpayers who argued the town’s 2024 revaluation — which led to increased tax bills — was conducted unfairly and unlawfully.

Making deposits at local banks means more money being reinvested in your community

There are no magic wands in tax disputes, but the current New Hampshire Department of Revenue Administration (DRA) tax amnesty program is about as close as it gets.