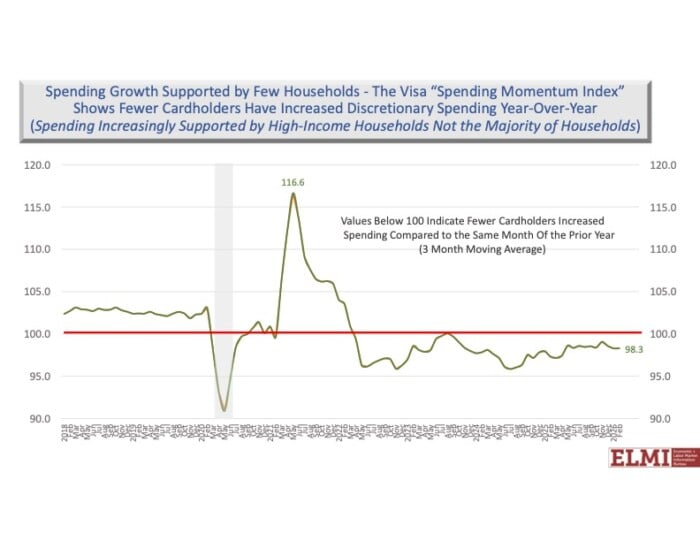

NH economist lowers forecast for 2026

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

Following annual reductions in both the Business Profits Tax (BPT) and Business Enterprise Tax (BET) between FY 2015 and FY 2022, Republican lawmakers have proposed a second, more expansive round of tax reductions between FY 2025 and FY 2030.

HB 1422, sponsored by Rep. Joe Sweeney (R-Salem) and co-sponsored by House Majority Leader Rep. Jason Osborne, called the Consumer Tax Relief Act, would reduce the rates of the two business taxes as well as the Meals and Rooms Tax, while trimming then repealing the Communications Services Tax in 2027.

The BPT, currently levied at a rate of 7.5%, would be reduced by 0.1% each year beginning in tax year 2025 until reaching 7% in tax year 2030. The BET, currently levied at a rate of 0.55%, would be reduced by 0.1% each year over the same period before returning to its original rate of 0.25% when it was introduced in 1993.

The Meals and Rooms Tax, which includes vehicle rentals, would be reduced from 8.5% to 6.0% between FY 2025 and FY 2027. Currently, 30% of the revenue from the tax is allocated to the Meals and Rooms Municipal Revenue Fund, which is distributed to cities and towns based on their population. The bill would increase the distribution to 42.5% beginning in 2025. However, the Department Revenue Administration projects that the reduction in the tax rate will shrink the amount deposited in the fund.

The Communications Services Tax would be halved from 7% to 3.5% for each month from July 2024 to June 2025 and halved again to 1.75% before being repealed on January 1, 2027.

The DRA provided a static analysis, which does not take into account the effect of the rate reductions on economic activity in the long term to estimate the fiscal impact of the bill. The department estimated that revenues from the four taxes would shrink by increasing amounts each year between FY 2025 and FY2031, and the cumulative fiscal impact would amount to $2.2 billion in foregone revenue.

Proponents of reducing taxes contend that lower taxes stimulate economic activity and growth, which in turn generates increased tax revenues. Last year Phil Sletten, research director of the NH Fiscal Policy Institute, undertook an extensive analysis of the fiscal and economic effects of reducing business taxes from FY 2015 to FY 2022. He reported he “found no evidence that concurrent business tax rate reductions led to increased revenue by spurring more economic activity in the state.”

Instead, he concluded that, by reducing business tax rates, the state failed to capture the revenue generated by the growth driven by other factors, forgoing between $496 million and $729 million in revenue between 2016 and 2022. Sletten’s report can be found at nhfpi.org.

Osborne, along with other sponsors of HB 1422, has also sponsored CACR 15, proposing to amend the Constitution to require a two-thirds majority to increase any tax or license fee, or to introduce a new tax or issue state bonds. A two-thirds majority of the Legislature is required to place the amendment on the ballot and a two-thirds majority of the electorate would be required to adopt it. Similar measures have failed in the past.

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

If nothing changes between now and then, the trust fund that finances Social Security payments will run out, triggering a 7% decline in monthly payments in 2032 and dwindling further to 28% from 2033 through 2036.

Our post-pandemic business environment has brought about myriad challenges that make cash flow forecasting much more difficult than it was five years ago. Many businesses are navigating supply chain challenges, volatile demand and lingering inflation — all key indicators of future cash flow.

Howard Brodsky, co-founder and chairman of CCA Global Partners (CCA), highlighted the power of cooperatives (co-ops) — shared business models owned and governed by their members — as the “great economic equalizer” for small businesses worldwide in his remarks at the United Nation’s (UN) annual Session of the Commission for Social Development at UN headquarters in New York City. This session convened global business leaders and innovators to discuss advancing social development and social justice through coordinated, equitable and inclusive policies.

Analysts fear overall revenue will lag unless other accounts pick up the pace

Analysts fear that once it’s gone for the remainder of the fiscal year, overall revenue will lag unless other accounts, which have been underperforming to date, pick up the pace

A judge has dismissed a lawsuit filed by more than 70 Hampton taxpayers who argued the town’s 2024 revaluation — which led to increased tax bills — was conducted unfairly and unlawfully.

Making deposits at local banks means more money being reinvested in your community

There are no magic wands in tax disputes, but the current New Hampshire Department of Revenue Administration (DRA) tax amnesty program is about as close as it gets.