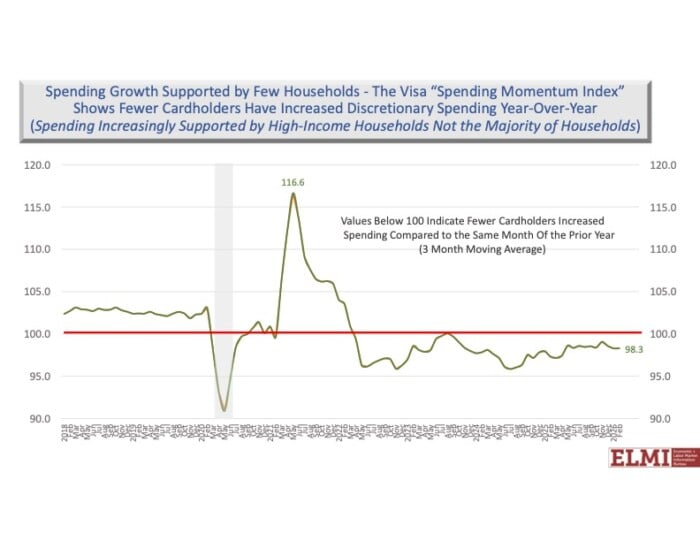

NH economist lowers forecast for 2026

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

Before co-founding Rise Private Wealth Management, Bob Bonfiglio started his career as an engineer. After spending a few years at Texas Instruments and Raytheon, he went on to receive his MBA to get into business for himself.

Before co-founding Rise Private Wealth Management, Bob Bonfiglio started his career as an engineer. After spending a few years at Texas Instruments and Raytheon, he went on to receive his MBA to get into business for himself.

When sharing his story on a recent episode of NH Business Review’s Down to Business podcast, Bonfiglio mentioned that his career pivoted after reading the book “What Color Is Your Parachute?” by Richard Nelson Bolles. After going through the exercises outlined in that publication, Bonfiglio led himself down a path where he would officially start Rise Private Wealth Management, an Ameriprise Private Wealth advisory practice in Bedford.

Q. With what you learned and the kind of skills you need to be an electrical engineer and work for companies like Raytheon, what from that experience helps you in wealth management?

A. I think a disciplined approach helps and something that to be objective. More of my learnings came from my leadership development journey and helping build the firm.

Back when I started in the business, it was brutal. It was a lot of cold calling, and you know, just brute force work hard and a lot of perseverance. Thankfully, today we’ve changed the model and how people can get into the career. I survived. It was about a 90% fallout rate when I started. So, I was one of the 10% that survived in the business.

I always wanted to be in leadership. And so that was my goal. I got into leadership pretty early on in my second year in the business and went on to be a field vice president with Ameriprise. About 15 years ago, I decided to go back into practice and build from there. And in 2010, I hooked up with Brent Kiley from Bedford, and we started Rise at that time. At the time we had seven people in the firm, including Brent and I. This morning we’re at 68, including eight interns, and we have offices in several states with seven offices in five states. And we work with people all over the country — about 4,000 families and businesses managing $2.6 billion in assets for our clients.

Q. In terms of remote working, you were already probably working that way before Covid, if you were already in multiple states.

A. Yeah, we were already working that way. Back in March of 2020, like many other companies, we had to convert to a remote organization, which was very challenging, especially for parents. Parents of school-aged children who were trying to work, trying to educate their kids with remote learning. That was challenging for many on our team.

So, we did some things to help our team and sending meals to them so they didn’t have to prepare meals, things like that. But from a business standpoint, we actually saw a boom in business. And one of the things was, normally when we want to have an appointment with a client they say, “Oh well, I’m traveling next week. I got a little league game the following day. Maybe we can meet in three weeks.” Well, during the pandemic, it was like, “how about tomorrow? I got nothing to do.” We were able to capitalize on that and make the most of a terrible situation.

Q. What is your leadership philosophy?

A. One of the things is, we have a strategic plan that we follow. We were exposed to a book called “Traction: Get a Grip on Your Business” by Gino Wickman about six years ago, and he developed the entrepreneurial operating system (EOS). We decided to follow that system, and as part of that, we developed a 10-year plan, a three-year plan, a one-year plan and a quarterly plan. As part of that, also have a vision, mission and values. We’re very strong on that.

We have four core priorities, and one of them is leadership development. Brent and I decided when we founded Rise that we wanted to be a firm that was here for generations to come for our clients. Not all advisory firms are like that. In order to do that, we needed to develop the next generation of leaders.

One of the things we try to do is never do meetings alone with our clients. When I’m on a meeting with a client, I’m always shadowed by someone who’s up and coming and developing in the organization, so they can take notes and help with the follow-up. And from that client, there’s always things going on in the meeting that the client needs done. So, they can actually get some of those things done during the meeting. But also, they’re observing me interacting with my client, and they’re learning from that.

Our new up-and-coming advisors spend most of their week being on meetings with me and others to learn the business, and then other parts of their week they’re in training, learning different aspects of the business.

We also have a formal leadership development program, and about 40% of our firm is in the program. During the formal monthly leadership training, (newer leaders) will learn things on how to do one-on-ones, things about change management, conflict management, etc.

Another thing we have put together is a mentorship program for up-and-coming executive team leaders. They’re hooked up with one of our current executive team members, and they have a mentorship meeting every month, not with their direct leader, but someone who’s another advocate for them in the organization that can help them develop over time. Also, our staff in the front of the house — those people that interact with clients every day — and in the back of the house with people that are in operations and doing some of the service work, they all have a very well-defined career track, so people know what it takes to win and to get to the next level. I believe that’s very important for retention and recognition of people that they know. What do they have to do to get to the next level to develop as a productive team member and eventual leader on the team?

Q. Tell us a little bit about your business model.

A. We have advisors who, like myself are in their early 60s. We have advisors in their 50s, 40s, 30s and 20s. One of our newest certified financial planners (CFP) is fresh out of college, 20-22 years old, probably one of the youngest people to have a CFP in the industry, because there’s very few actually under 30 that have CFP.

The money is skewed to people that are probably 50 and older. So, I personally work with people that are closer to retirement, but some of the other team members work with younger professionals.

We have a segment of our team that works with clients that are $5 million to $25 million in assets. We have a segment of our team just getting started that works with people who are also getting started.

We’re in the money business, so the more that you have, the better it is. But it’s really focused on value-based planning. We put an emphasis on behavioral finance, which is connecting your values and your goals and your actions. In our industry, as people oftentimes react very emotionally to ups and downs in the market, part of our role is to make sure that their actions are connected to their goals and their values, and they don’t make moves that are counter to those.

So really taking time to understand that up front with our clients is really important. We also do a values exercise with each of our employees as well. Part of our leadership model is to do what’s called a WYFY: what do you want for yourself? Everyone completes a values exercise, so I understand what’s important to you. And then we talk about: what are your goals in the next 90 days, one year, three years, five years? what do you want for yourself professionally? what do you want for yourself personally? what do you want for yourself? for your family? We want to understand that, so we can help you achieve that.

If you look at the most common values for people worldwide, it’s family, health, happiness. One of my values and our team values is philanthropy. When working with multiple generations of a family, it gives them comfort knowing that there’s some consistency and succession with their assets that are going to get used in a good way.

Q. During succession, when a company is going to sell either to someone else in the family or they’re selling, what is the role of CFPs?

A. I work with a lot of business owners, and many of them think that the business is just themselves and when they go away, there’s no more business. And what I try to educate them on is that, yes if that’s how they’ve arranged things, then they’re exactly right. One of the big influences in my career has been a book called “The E-myth Revisited” (by Michael E. Gerber). And the entrepreneurial myth (e-myth) is when you’re an entrepreneur and you start a business, life’s going to be glamorous; you’re going to get rich automatically; things are going to work out rosy. And of course, what many business owners find out is that, instead of having control over their life when they start a business, the business controls them and they’re working 100 hours a week and they can’t make ends meet.

One of the principals in that book was, if you’re going to take the trouble to be a business owner and own a business and run the business, then you might as well run it. You might as well build it to sell, so that at some point you’re able to capitalize on it. If you’re not interested in selling it, then why build it? why not just work for somebody else? why go through the pain, agony and torture of owning the business? where’s your investment? I took that to heart.

When I came into practice in 2007 and started building the business, that’s when I hooked up with Brent. I was in my mid-40s and he was about 30ish. We had similar values, similar vision, similar goals but different skill sets that complemented each other. So, we began to work together, and at first, the biggest reason to work together was that I’d have somebody — you know, God forbid, if I got hit by the bus — that he would help me with my clients. If he got hit by the bus, I would help him with his clients and his team, and we’d have succession there. So, we had a formal succession plan.

I don’t see a lot of business owners doing this in the community. Even if they’re on their own, like I did, I found someone else in my industry that could do a cross agreement: something happened to me, he takes care of my family; something happens to him, I take care of his. So even if you’re in construction or some other kind of business, you can still do that. That’s the first step of succession.

We talk in our company about the certainty of uncertainty. When we plan for people, we can plan for good markets, but we should also plan for poor markets. We plan for good health, but we should also plan for bad health or premature death. And we always want to have a smart place where money is located so that, God forbid the unplanned event happens, we can still move on and the business can still thrive.

Second step is try to arrange your business so that it can operate without you. If your business can operate without you, how much more valuable is that to a potential buyer? And it’s a sellable business now, because you don’t have to be there to operate it.

We have a self-functioning team, and I’m no longer the CEO. Brent’s the CEO, and we have a whole executive team running the business, which I’m part of, but it’s not reliant on me. Of course, I’m a major contributor, but if I went away today and retired, the business would thrive without me. That’s an aspirational point to be for any leader. Your business is going to be worth way more if you don’t have to be there to operate it.

Q. Can you share some insight into how to continue growing as a leader.

A. In my tenure with leadership, I was a field vice president with Ameriprise and I’ve worked with many business owners in the community and around the country. And what I’ve observed from business owners and entrepreneurs that are highly successful is that they have a very compelling vision backed by a mission and values that they share with the team — that compelling vision that pulls you, that stretches you and causes you to strive to be better.

The second thing is they’re willing to take risk, and they’re willing to do what’s uncomfortable for them to grow. Growth and comfort don’t go together. Yeah, growth is uncomfortable, but successful entrepreneurs are willing to take that risk.

And the third thing that I find really key is to reinvent yourself and reinvent your business every two to three years. So, I’m playing a role today that I wasn’t playing three years ago. Three years ago, I was playing a role I wasn’t playing three years before that. And because I’ve developed people behind me, I’m able to do that.

With the business, every few years as it grows, it runs into a ceiling. And you have to reinvent to break through that ceiling for more growth.

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.

If nothing changes between now and then, the trust fund that finances Social Security payments will run out, triggering a 7% decline in monthly payments in 2032 and dwindling further to 28% from 2033 through 2036.

Our post-pandemic business environment has brought about myriad challenges that make cash flow forecasting much more difficult than it was five years ago. Many businesses are navigating supply chain challenges, volatile demand and lingering inflation — all key indicators of future cash flow.

Howard Brodsky, co-founder and chairman of CCA Global Partners (CCA), highlighted the power of cooperatives (co-ops) — shared business models owned and governed by their members — as the “great economic equalizer” for small businesses worldwide in his remarks at the United Nation’s (UN) annual Session of the Commission for Social Development at UN headquarters in New York City. This session convened global business leaders and innovators to discuss advancing social development and social justice through coordinated, equitable and inclusive policies.

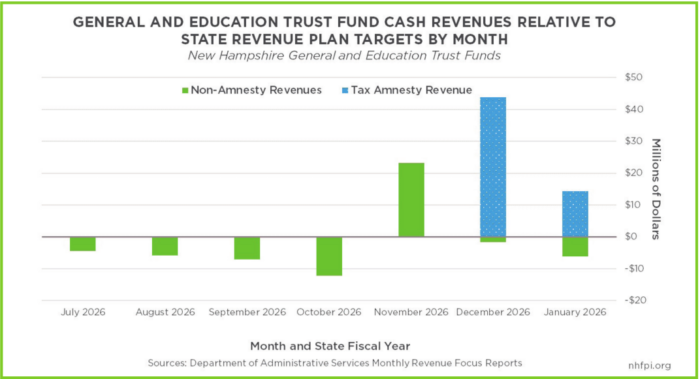

Analysts fear overall revenue will lag unless other accounts pick up the pace

Analysts fear that once it’s gone for the remainder of the fiscal year, overall revenue will lag unless other accounts, which have been underperforming to date, pick up the pace

A judge has dismissed a lawsuit filed by more than 70 Hampton taxpayers who argued the town’s 2024 revaluation — which led to increased tax bills — was conducted unfairly and unlawfully.

Making deposits at local banks means more money being reinvested in your community

There are no magic wands in tax disputes, but the current New Hampshire Department of Revenue Administration (DRA) tax amnesty program is about as close as it gets.