Navigating your financial journey in wealth and trust planning

Whether you are planning for long-term growth, managing income needs, or preparing the next generation, wealth management often involves balancing multiple priorities.

A judge has dismissed a lawsuit filed by more than 70 Hampton taxpayers who argued the town’s 2024 revaluation — which led to increased tax bills — was conducted unfairly and unlawfully.

The group, led by former selectwoman Regina Barnes Player, represented themselves during a Jan. 8 hearing in Rockingham Superior Court.

While Judge Lisa English credited the plaintiffs and their supporters at the hearing for their strong civic engagement, she advised at the time she could only weigh in on the motion to dismiss. Two weeks later, Jan. 21, she handed down an order granting that motion.

Barnes Player posted a link on her blog to her group’s response, including that they filed a motion for reconsideration with the judge. In both the post and the filing, she argued the judge did not address the core issues raised in the lawsuit.

“Did the town of Hampton even have the lawful authority to send out property tax bills at all?” Barnes wrote in the post. The lawsuit was in response to the recent townwide property revaluation that had Hampton property values increase by an average of 53%. Property values rose across the region in revaluations conducted in virtually all local communities.

The suit alleged state lawmakers and agencies are enabling a system that allows property values to be assessed based on “market value,” which they argue is arbitrary and unfair. It further alleged “civil conspiracy” and “fraud,” and described the appeal process through the state Board of Tax and Land Appeals as a “bait and switch scheme” that prevents taxpayers from challenging the actual assessed tax amount.

The suit argued that the town’s 2024 revaluation disproportionately impacted certain properties — particularly those near the beach — because it was based on a statistical analysis of recent sales rather than a full “measure and list” revaluation.

A measure and list revaluation involves physically visiting every property in town to measure the exterior of the building and list all relevant property details. According to the suit, the last such comprehensive review in Hampton was conducted between 2008 and 2010 and covered only 40% to 60% of properties.

The town’s motion to dismiss argued the superior court lacks jurisdiction over property tax assessments and most tax abatement matters. Citing RSA 71 B:5, the town attorney wrote that only the Board of Tax and Land Appeals has the authority to hear reassessment claims, and only in a non appellate capacity.

The town attorney also argued that taxpayers can only bring a case to the superior court only after the Board of Assessment, or Select Board, and the Board of Tax and Land Appeals have denied an abatement request. She said that only a limited number of petitioners in this suit actually filed an appeal with the Board of Tax and Land Appeals. Those cases were heard in April 2025 and still await a decision.

English, in her Jan. 21 decision, agreed with the town’s position the lawsuit was filed prematurely because the taxpayers had not completed the required town and state abatement processes. Under state law, she noted, taxpayers must first seek relief through the town and then the Board of Tax and Land Appeals before turning to the superior court.

She added that the window to request a 2025 abatement through the town remained open, while the deadline to seek an abatement for 2024 — the year at issue in the suit — had already passed.

English also agreed with the town’s argument the plaintiffs had not shown any basis for their claim under the federal Racketeer Influenced and Corrupt Organizations Act, a statute most commonly associated with prosecuting organized crime.

To allege fraud, she wrote, plaintiffs must show that a defendant “intentionally made materially false statements to the plaintiff, which the defendant knew to be false or which he had knowledge or belief to be true.” In this case, she concluded, “there are no allegations that plaintiffs relied on any alleged false statements by the town in the collection or determination of property taxes.”

Barnes-Player said she and her fellow plaintiffs are working on their next steps. She has said that many residents are struggling to stay living in town as taxes continue to rise.

The court did not rule on the claims the plaintiffs actually presented,” Barnes-Player wrote in the motion for reconsideration, filed the same day as the order to grant dismissal.

Barnes-Player wrote in the motion that her group did not seek a reassessment, abatements or review of valuation mathematics, but rather a “declaration that the town acted without lawful authority.” She said her group is also working to bring their case to the state and the U.S. Supreme Court.

“Plaintiffs challenged the power to tax. The court responded as if they challenged the accuracy of the tax,” Barnes wrote. “That maneuver doesn’t resolve the dispute — it sidesteps it.”

Whether you are planning for long-term growth, managing income needs, or preparing the next generation, wealth management often involves balancing multiple priorities.

At Blueline Advisors in Exeter, chief investment officer Frank Sabin is embracing AI, with the help of the students, to better serve his clients, who have entrusted about $250 million in assets in his care.

Successful investing takes a lot of patience. Risk tolerance and time horizon are important factors in determining an appropriate investment strategy. For example, some investments would be unwise to choose if the principal is…

During the last three months, hundreds of thousands of Granite Staters filed federal income taxes for Tax Year 2025.

Business growth is exciting. A big contract comes through, a new customer relationship takes off or marketing is delivering the results you expected. Financing can be a critical resource to sustain the growth. But from a lender’s perspective, growth financing is about more than momentum. The real question is whether the business can support that growth — and repay the debt that may come with it.

Fidelity Investments announced Wednesday that New Hampshire is one of four Fidelity sites that will transition to a full-time, on-site schedule beginning in September

After two choppy years for dealmakers, 2026 is starting with a very different tone, one that many business owners have been waiting for. While the past few years brought tariff swings, interest rate volatility and a cautious lending environment, the fundamentals are shifting in a way that increasingly favors sellers, especially those in the lower-middle-market (LMM).

Today’s consumers don’t just want convenience. They expect it, whether it is speed, digital tools, quick answers, and the ability to do routine tasks from their phones.

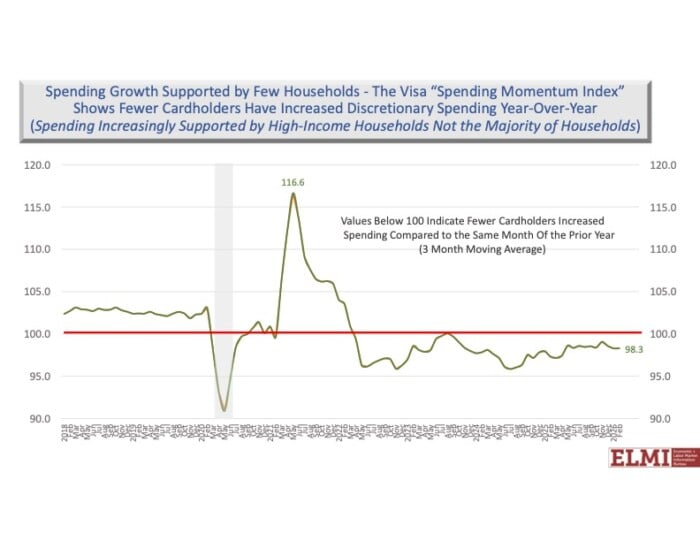

A key New Hampshire economist has trimmed down to 2.2% his forecast for the growth in the state's economy this for 2026, citing lackluster consumer confidence and the uncertainty of the U.S. war against Iran.